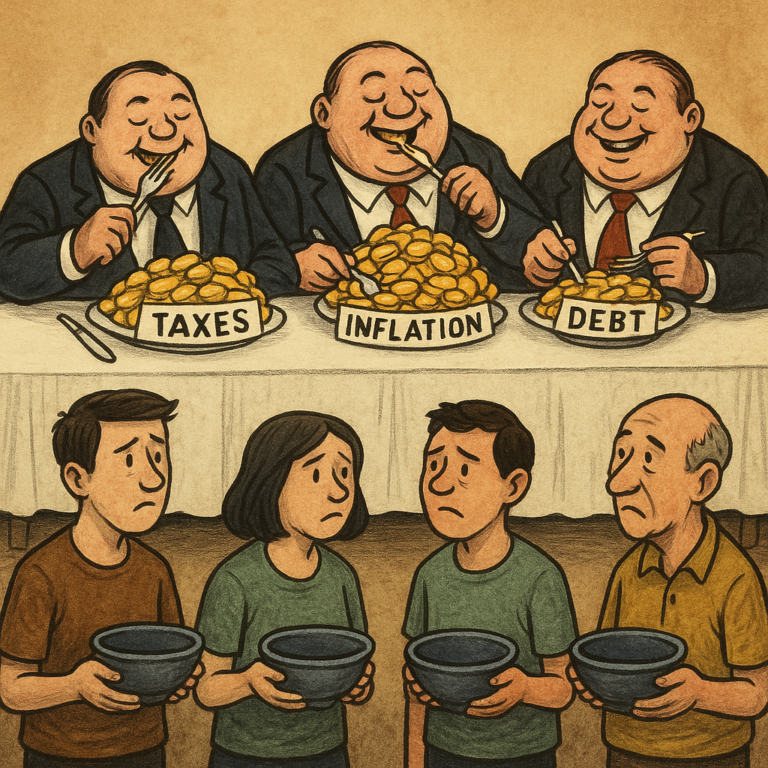

Debt is a bet on your future—and a leash around your neck.

All Debt Is a Claim on Future Time

Every dollar you borrow is a claim on hours you haven’t lived yet. It’s not free—it’s your future, sold at a discount. You’re pledging time you haven’t spent, labor you haven’t performed, and freedom you haven’t used.

Debt may buy comfort in the short term, but it mortgages your long-term sovereignty. It delays pain now by guaranteeing servitude later.

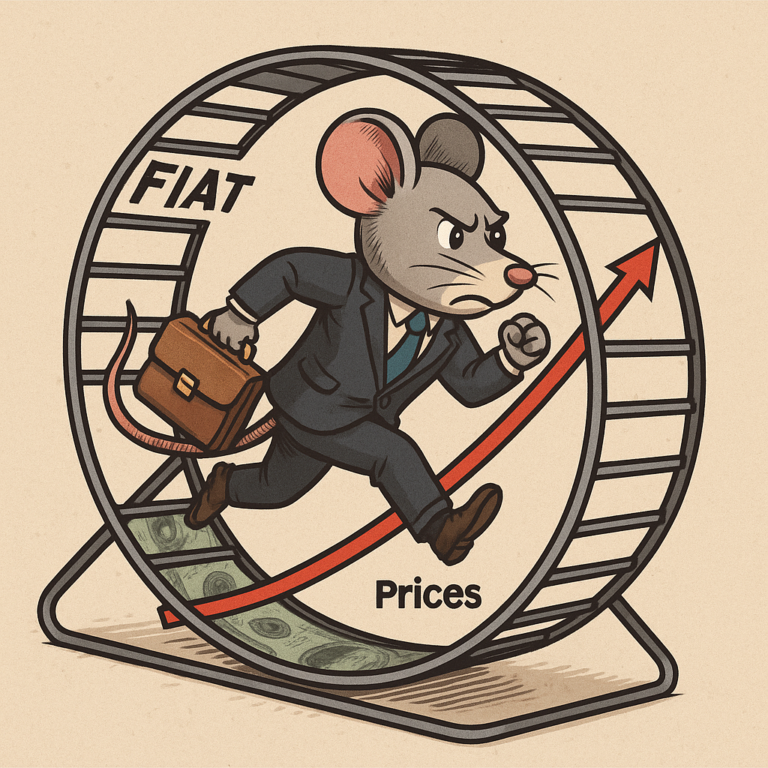

Debt Assumes Tomorrow Will Be Better—But Inflation Ensures It Won’t

The entire fiat system depends on an assumption: that tomorrow will be more prosperous than today. Only then can growing debts be paid back. But this optimism is undermined by inflation, which eats away at purchasing power and undermines savings.

As inflation rises, the real value of wages stagnates. Servicing debt becomes harder—not easier. The promised “better tomorrow” keeps moving further away.

Mortgages Are Not a Sign of Prosperity—They’re a Symptom of Decline

We’re taught that a mortgage is a smart financial decision. But the reality is more sobering: the average person needs to borrow for 30 years just to afford a roof over their head—not because homes are intrinsically expensive, but because fiat money has made saving worthless.

In a sound-money system, where currency retains its value over time, most wage earners would be able to save for and buy a home outright within a reasonable number of years. Mortgages aren’t a sign of economic health—they’re proof that savings can’t keep up.

A Mortgage Is Debt Slavery Dressed Up as Ownership

You don’t own your home until the mortgage is fully paid. Until then, the bank does. And if you stop paying, they’ll take it back—no matter how much equity you’ve built up.

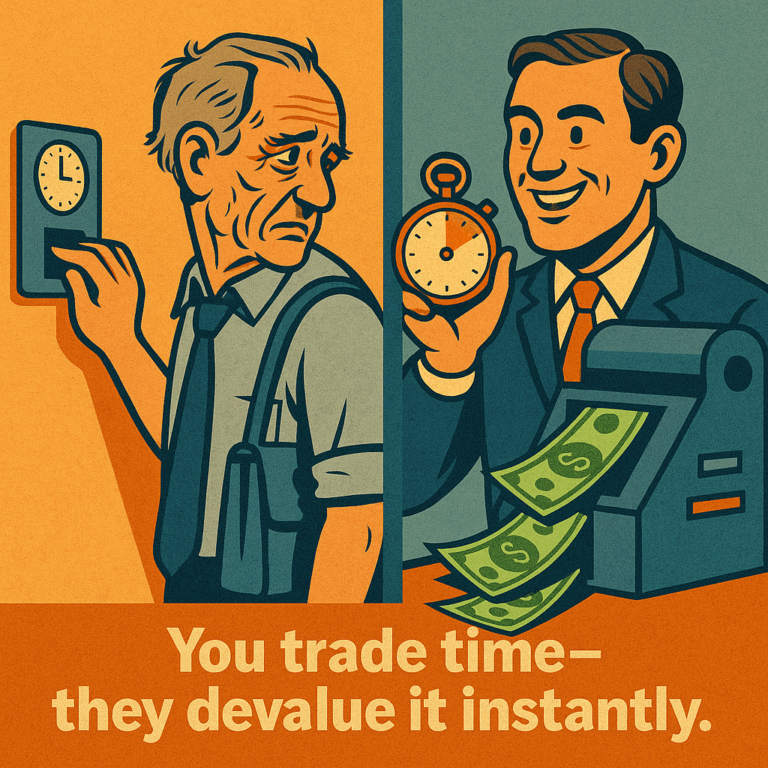

What’s worse: the bank didn’t have to earn the money they lent you. They created it with a keystroke, using fractional reserve banking to conjure dollars out of nothing. You, on the other hand, have to exchange decades of labor to pay it back—with interest.

You’re working for the bank. They’re printing for themselves.

Retail Borrowers Get the Worst Deal

The interest rates you pay on mortgages, student loans, and credit cards are a far cry from the rates big players get. Institutional borrowers and politically connected entities can access near-zero interest loans. You, the retail borrower, are stuck paying 6%, 12%, or more.

This isn’t a fair game—it’s a hierarchy. And the deeper in debt you go, the more power the system has over you.

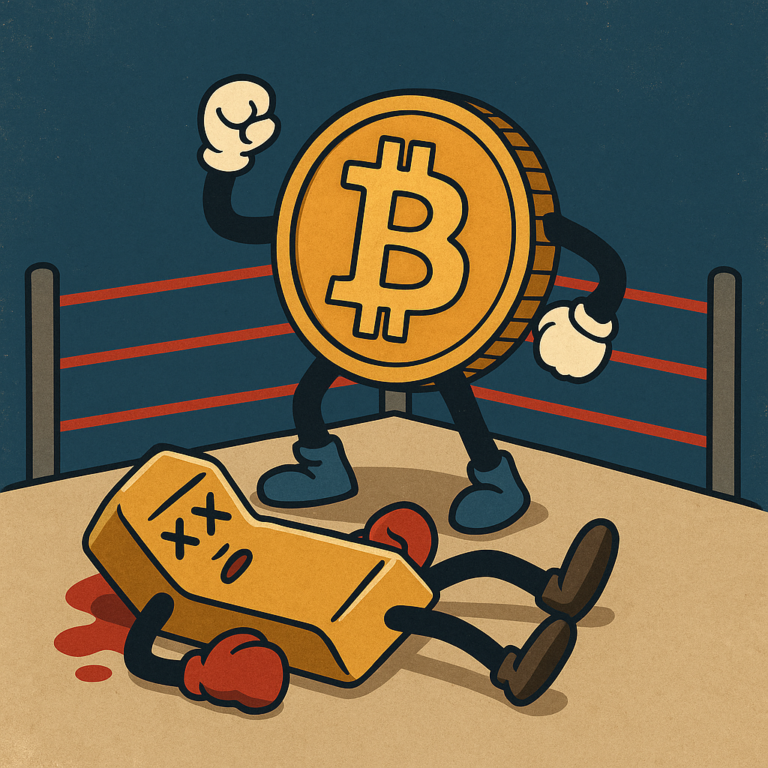

Bitcoin Ends the Debt Delusion

Bitcoin doesn’t inflate. It doesn’t reward debtors or penalize savers. It aligns present action with future security. And it offers an exit from a world where freedom is collateral for fake money.

In a Bitcoin world, the dream isn’t to leverage yourself to the hilt—it’s to own outright. It’s to build, save, and rest without perpetual repayment.

The Bottom Line

- There’s no such thing as “good debt”—only socially accepted bondage.

- You don’t own a mortgaged home—the bank does. And they created the money you’re repaying out of thin air.

- Bitcoin offers a path to real ownership—earned, not borrowed.