Why You Should Care

The average person who works 40hrs per week, 48 weeks per year, for 45 years of their life, will spend 86,400hrs of their life working for money. Yet most will go their whole lives without spending a single hour learning what money actually is. This page aims to give you a solid foundational understanding of money in LESS than 20 minutes. To do that, first we’ll look at why money emerged, the various forms it’s taken throughout history, and the criteria for what makes something useful as money. Let’s begin…

Discovery of Trade

We are all mortal human beings, and as such we all have needs. Many of these needs require some combination of time, energy, and resources to fulfil. When faced with an unmet need, you can either attempt to fulfil it yourself, or seek the help of another who may be better equipped to fulfil that need for you.

If you choose to fulfil a personal need independently, you will expend time, energy and resources that could have otherwise been directed towards another of your unmet needs. This creates an ‘opportunity cost’ associated with fulfilling any personal need yourself. The degree of this ‘opportunity cost’ depends upon your individual efficiency of fulfilling that particular need. The less efficient (or apt) you are at fulfilling that need, the greater your opportunity cost will be.

If you choose instead to fulfil a personal need through the service of another person, you are effectively imparting this opportunity cost onto them. They will be expending their own time, energy and resources to fulfil your need, which they otherwise could’ve spent fulfilling their own needs.

Excluding acts of charity, a rational helper will feel this opportunity cost and expect a reciprocal favour from you, of satisfactory magnitude, in exchange for their services. To satisfy this expectation, you may wisely offer to help them fulfil one of their personal needs. In fulfilling this need, you will have engaged in a form of trade with that person known as ‘barter’.

In general, trade is mutually beneficial when the opportunity cost of fulfilling each other’s needs is lower than it otherwise would have been if you’d both fulfilled your needs individually. In other words, mutual trade occurs spontaneously and voluntarily when both parties are more efficient at solving each others’ problems than they would be at solving their own. This creates a win-win situation, or a ‘positive-sum’ interaction.

As mortal humans, we are driven to survive and improve our condition. Therefore, there’s a powerful incentive to find opportunities for consensual, mutually-beneficial trade. The more efficiently we can trade with each other, the better our standard of living. In short, humans discovered that they could mutually benefit from exchanging value. This incentive led humans to specialise according to their own innate talents and abilities; a practice known as ‘division of labour’.

Since human ability varies widely across myriad domains, opportunities for mutually-beneficial exchange always exist. However, finding such opportunities when you’re in need is not always easy or practical. It would necessitate you finding someone who coincidentally wants what you have to offer, and is willing to give you what you need in return. This is known as the ‘coincidence of wants’ problem, and is one of the inefficiencies inherent to barter. Over time, humans have devised multiple solutions to this problem.

The History Of Money

In more primitive times, prior to the discovery of money, one solution to this problem was ‘social credit’, or reputation. For example, if you made a kill on a hunt, but your neighbour did not, you could share your excess food with him. In receiving this food, your neighbour will remember this favour, and be more willing to share future food with you in the event that he makes a kill and you do not. Alternatively, these favours could be recorded in other ways, such as physical ledger markings on cave walls, or as rank in a tribal hierarchy. Regardless of method, this solution of ‘storing’ favours as reputation was effective in honest, tight-knit communities, however it became unreliable at scale.

As human societies grew in size, people instead began to preferentially trade their favours for a range of staple items that everybody commonly seemed to want. Such commodities like salt, spices, tobacco, grain, flour and coffee emerged as ‘intermediate goods’ that people would store in ‘caches’, not to be consumed personally, but ready to be traded later for the favours they actually wanted. ‘Commodity monies’, as they’re now known, were effective ‘mediums of exchange’ because they were commonly demanded, easily divisible, and easy to physically authenticate. Some were also reasonable ‘stores of value’ since they were slow to spoil and relatively hard to counterfeit.

Commodity monies, however, also had limitations. Whilst some were slow to spoil, most still had a shelf life, meaning they would depreciate with time and eventually require consumption if not traded. Another limitation, was a lack of standardisation in quality, and therefore consistency of trade value, of any given commodity. There were also limits to how much of any given commodity an individual would reasonably want to store. This meant that individual preferences for any given commodity would vary from person to person. And finally, there was the inconvenience of needing to transport bulky quantities of various commodities to wherever potential trades might occur.

As civilisation progressed, people were able to produce larger and larger quantities of the staple commodities being used as money. Thanks to basic technology and agriculture, the supply and availability of commodity monies rose significantly, and their monetary value consequently declined. At the same time, the demand for certain metals, like gold, silver, bronze and nickel, was rising.

As the demand for certain metals rose, so too did their tradable (monetary) value in the marketplace. As the ‘monetary value’ of these metals increased, so too did the incentive to mine and refine more of them. Any metal that was plentiful in the ground, or would corrode quickly once refined, soon ceded monetary value to metals that were more scarce and durable. A small handful of metals – namely gold & silver – that were scarce and durable enough, consolidated all remaining ‘monetary value’, and so began the age of ‘metallic money’. The metal with the highest scarcity and durability was gold, and it consequently reigned as the dominant store of value for several thousand years.

Gold became money not because someone declared it so, but because it inherently possessed several key qualities that made it superior in its monetary function. Firstly, it was reliably scarce, difficult to acquire or counterfeit, and therefore resistant to inflation. Second, due to its chemical inertness, it was extremely durable and could be held indefinitely without degrading. Third, it was easily recognisable and quantifiable at point-of-trade, particularly when standardised in coin form. And finally, it had high value-density, making it far more portable than earlier commodity monies like flour and salt.

Unfortunately, gold also had its limitations. For one thing, its limited divisibility and high value-density necessitated the use of a secondary metal money (silver) for lower-value transactions. Additionally, the periodic issuance of coinage by rulers provided an opportunity for them to quietly steal money from the people through dilution (‘debasement’) of a coin’s gold/silver content. The resulting inflation was the common denominator for much human suffering, and many collapses of great empires throughout history. And finally, gold’s physicality made it a prime target for theft. All a bandit had to do to acquire someone’s gold was dominate them with force or cunning.

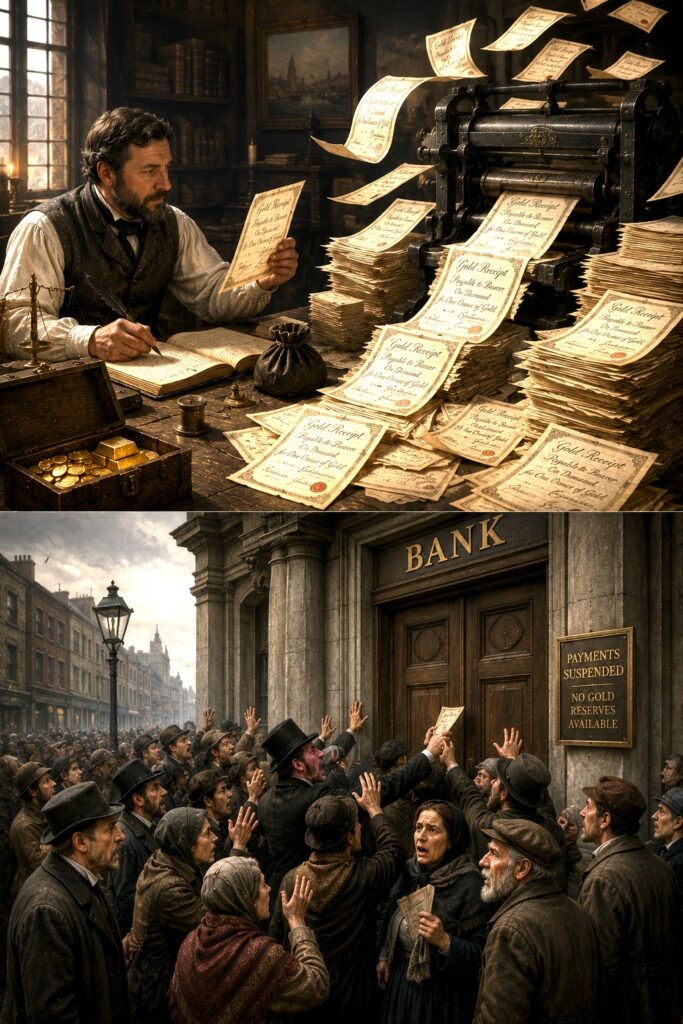

To mitigate the risk of theft, gold custodians emerged, offering to safely store a depositor’s gold in exchange for a small fee. Upon deposit of one’s gold, the custodian would issue a paper receipt, which upon return, would be redeemable for the stated amount of gold.

These gold receipts were ‘bearer assets’, meaning anybody who bore the receipt could redeem the stated amount of gold from the receipt’s issuer. This transferability allowed people to trade gold receipts (rather than physical gold) for goods and services.

In this way, gold receipts became the prototypical ‘paper money’, and they increased the efficiency of trade significantly. However, by abstracting the value of the underlying gold into paper form, the new problem of ‘counterparty risk’ emerged. Bearers of the gold receipts now had to trust that the custodian held enough gold in reserves to satisfy potential redemptions.

Once gold receipts had gained traction through their utility as a ‘medium of exchange’, they tended to stay in circulation rather than be immediately redeemed. Gold custodians soon realised that only a fraction of outstanding receipts were ever redeemed at the same time, and there was always idle gold sitting in their vaults.

This idle gold presented custodians with a two perverse incentives; to either a) issue more receipts than they had in gold, and/or b) lend out some of their customers’ gold to generate interest. Both practices inevitably led to custodians holding only a fraction of their outstanding gold receipts in physical gold reserves. This was the emergence of ‘fractional reserve banking’.

Fractional reserve banking caused numerous problems. Firstly, by issuing more gold receipts than what existed in physical gold, custodians (aka ‘banks’) artificially increased the supply of money in local economies. This ‘inflation’ of the money supply led to rising prices and rising costs of living. Secondly, there was always the risk that if enough people sought gold redemptions at the same time from an over-fractionalised custodian, that custodian would go ‘bankrupt’.

Whenever a custodian (bank) failed in this manner, anyone left holding their savings in that bank’s outstanding receipts got wiped out. Anyone who managed to redeem their gold in time would inevitably deposit their gold back into a different, seemingly ‘healthier’ bank, unaware that it also operated on fractional reserves.

From the moment ‘money’ was abstracted into paper form, the power to ‘print money’ became an irresistible magnet for governments, sovereigns, and bureaucrats alike. Over time, through a combination of bankruptcies, consolidation events, and political capture, governments acquired territorial monopolies over the power to issue currency.

The result is what we see today – all banks in any given country now deal in their national currency (rather than issuing their own bank notes), and all are now subordinate to their respective government’s ‘central bank’. Moreover, unlike the bank notes of old, fiat currencies are no longer redeemable for fixed quantities of gold. This de-coupling of currency (fiat) from money (gold) allows governments to ‘print’ as much currency as they wish, without limitation, and pass the cost to their citizens in the form of inflation.

This form of government-issued currency, unbacked by anything of value, and imposed through ‘legal tender laws’ and coercion, is known as ‘fiat currency’. Fiat currencies are the dominant medium of exchange in modern societies, not by merit or choice, but by government mandate. No longer can the people choose for themselves which form of money suits them best, or opt out without fear of violence or incarceration.

Despite the fact that currency is now ‘regulated’ by government, the modern banking system is no less precarious or immoral than the unscrupulous gold custodians of old. “Money” is still being printed, public debt perpetually grows as it’s rolled over, and society is subjected to the ongoing non-consensual wealth transfer of inflation.

By any logical definition, the fiat currency you’re forced to use today is not ‘money’, but rather an illusion of money imposed upon society. For something to count as ‘money’ it must first be consensually adopted by a free market on the merits of its monetary properties. Fiat currency fails this first test and therefore cannot be considered ‘sound money’.

Sound Money

‘Sound money’ can be defined as the intermediate good that’s naturally selected (without coercion) by the free market, that best performs the three functions of money (store of value, medium of exchange, & unit of account), and best satisfies the five properties of money (divisibility, durability, portability, recognisability, & scarcity).

Gold emerged as sound money because it satisfied these criteria better than anything else at the time. Interestingly, the term ‘sound money’ came about due to the characteristic sound that a gold coin made when dropped or struck against a hard surface.

Goods in any marketplace naturally compete with each other (in the minds of market participants) for the status of sound money. For a good to emerge as sound money in a free market, it has to perform three monetary functions better than any other good.

3 Functions of Sound Money

The first function is as a ‘store of value’, which is a good’s ability to retain its purchasing power over time. How well something holds its purchasing power over time depends upon its relative scarcity, and how reliably scarce it is over time. All else being equal, a good with sufficient scarcity, combined with a high difficulty or cost to produce more of, will tend to store its value best across time.

The second monetary function is as a ‘medium of exchange’. For a good to be a reliable medium of exchange, enough people in the marketplace must be voluntarily willing to accept it as payment for goods and services. All else being equal, the more effective a good is as a store of value, the more people will be willing to accept it as payment for trade, and the greater its effectiveness as a medium of exchange.

The third function of money is as a ‘unit of account’. When an intermediate good organically becomes the universal denominator of prices in a marketplace, it has achieved ‘unit of account’ status. For example, in a marketplace where all prices are voluntarily expressed by merchants in ounces of gold, then gold is the unit of account. All else being equal, the more people willing to accept a particular good as payment in a marketplace, the more likely that good is to denominate prices in that market, thereby becoming the ‘unit of account’.

Note:

Crucially, for a good to be a genuine medium of exchange and unit of account, merchants must voluntarily denominate their prices in that good, rather than be coerced by legal tender laws. As such, the fiat currencies that dominate world trade today cannot rightfully claim ‘medium of exchange’ or ‘unit of account’ status.

How well a good performs each of the above three functions of money, is a product of how well it satisfies the following five monetary properties, relative to everything else.

5 Properties of Sound Money

Divisibility

The first desirable property of money is ‘divisibility’, and it refers to the ease with which a good can be accurately metered out as payment, with minimal need for change. Being divisible allows it to be traded with ease, and maximises the fairness of any trade. Cows, for example, never became money because they aren’t practically divisible, whereas salt was. Interestingly, this is where the word ‘salary’ comes from.

Durability

The second requisite property of money is ‘durability’, referring to its ability to persist across time without rotting or deteriorating. All else being equal, a durable money is more likely to hold its value than one which rusts, spoils or degrades over time. Gold was highly durable due to its inert chemical nature, and did not deteriorate like other metals, which tarnished and rusted over time.

Portability

The third monetary requirement is ‘portability’. Given that money has to be transported to the point of sale, the more portable it is, the easier it is to carry and trade. Portability is a function of a good’s value-density, which is the measure of its market value relative to its size and weight. All else being equal, the easier a good is to carry, and the higher its value-density, the more portable it is as money.

Recognisability

The fourth monetary property is a good’s ‘recognisability’. A money with a high degree of recognisability means it is easy for trading parties to determine whether the money is real or fake. Given that money is valuable, there’s a constant incentive for people to make more of it, or substitute it with an imposter good that’s cheaper and easier to produce. Therefore, it’s desirable that a money be easy to authenticate as genuine, at point of sale, and by anyone with minimal training or tools.

Scarcity

The fifth and most important property of money is ’scarcity’. For a good to hold its monetary value across time, it must be reliably scarce in its supply. Ideally, its scarcity should also be independent of its geographic location. In some primitive societies, shells and glass beads have previously been used as money. However, technological advances made it easy for people to find large quantities of shells, and mass produce glass beads, such that these items collapsed in value. For something to be reliably scarce, it must either have an absolutely fixed supply (eg. bitcoin), or it must at least be very difficult to create/find more of (eg. gold).

Why Fiat ≠ Money

Contrary to modern economic doctrine, fiat currency does not qualify as ‘money’ for the following reasons…

Bitcoin = money

Bitcoin, on the other hand, is a nascent global money, which fully satisfies all five properties of sound money.

Bitcoin is Actively Monetising

Since bitcoin is infinitely divisible, perfectly durable, completely portable, inherently recognisable, and absolutely scarce, it has already begun the organic process of ‘monetisation’. Whenever a tradable good has undergone monetisation in the past, it has always followed the stepwise ascension through the 3 functions of money – 1) store of value, 2) medium of exchange, and 3) unit of account.

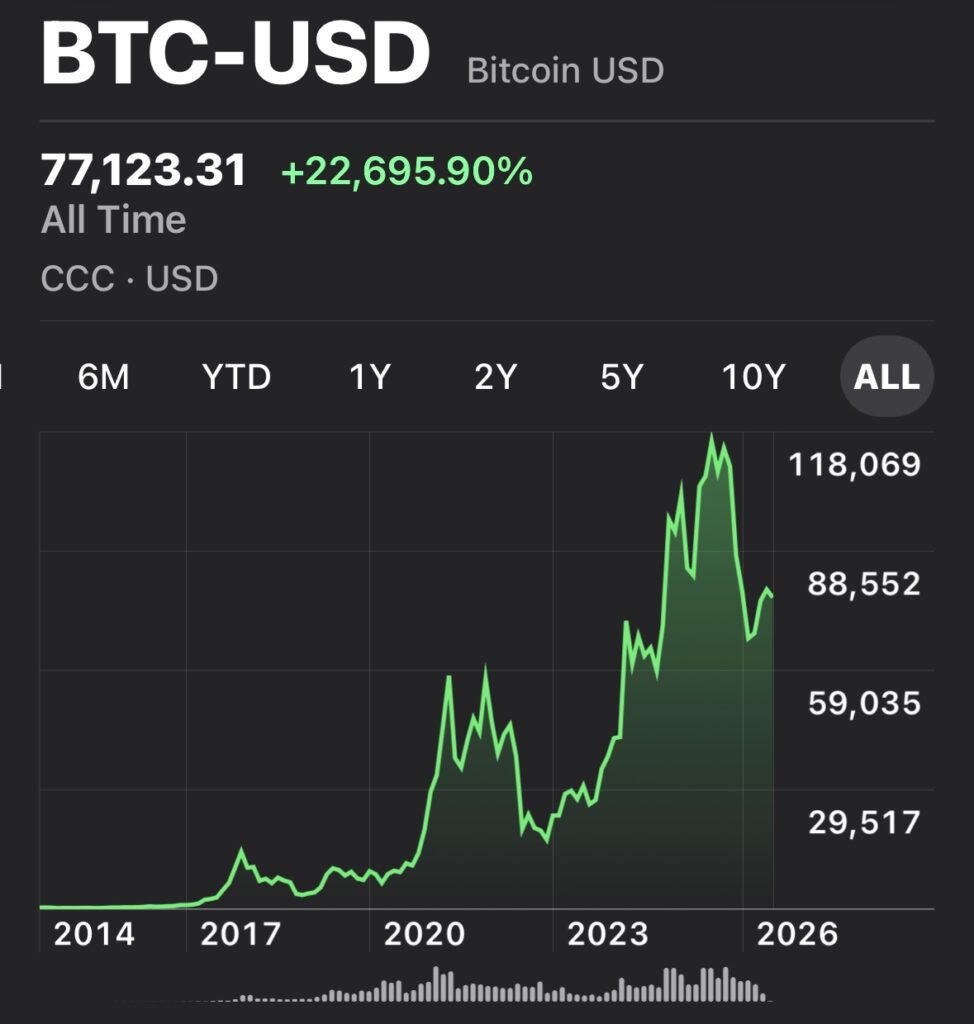

Bitcoin’s perfected monetary characteristics have caused many who’ve encountered it to realise its potential, and choose to use it as their store of value. Since bitcoin’s inception, there has never been a person who’s held bitcoin for more than 4 years and seen it depreciate in value. Thus, bitcoin is proving itself to be not just a reliable store of value, but the fastest appreciating new money in history.

There are also growing and emerging markets around the world where bitcoin is becoming the preferred store of value, medium of exchange, and unit of account. Whilst still small in number, the significance of people voluntarily forming circular economies running on bitcoin cannot be overstated. All else being equal, the more people who choose to use bitcoin as their preferred store of value, the more people who will be willing to accept it as a medium of exchange. Likewise, the more people willing to accept bitcoin as payment, the more goods and services will become denominated in bitcoin as the unit of account.

Bitcoin is early in this positive feedback loop, where adoption still seems slow relative to the number of people on Earth. However, given that the growth thus far has been organic, voluntary, and in spite of active suppression and mainstream misinformation, it’s logical to expect bitcoin’s adoption to accelerate as it continues to monetise and accrete value. Finally, if bitcoin has already surpassed $100k USD per BTC with less than 1% global adoption, what will it be worth when it’s fully monetised and is the world’s unit of account.

Food for thought.

Bitcoin First Principles

Continue your learning by clicking the next section below (Austrian Economics).

Leave a Reply